Investments | 26 September 2022

the bear necessities: what are bear markets and are there opportunities for investors?

Coutts Asset Management examine what markets moving in bear territory means for investors and how they relate to the broader economic outlook as well as how they can provide opportunities.

SHARE

Become a client

When you become a client of Coutts, you will be part of an exclusive networkBear markets are defined as sustained periods of downward trending stock prices, typically triggered by a 20% decline from recent highs. We saw this in June when the US S&P 500 officially entered a bear market for the first time since March 2020. Since then, we have seen a recovery of sorts but as of the year to 11 August the S&P 500 was down 11.7%; the FTSE 250 of UK mid-cap companies was down 13.7% and the Stoxx Europe 50 index was down around 12.9%.

WHY ARE WE IN ONE?

Inflation is now at its highest level in 40 years, creating high uncertainty with regards to economic outlooks. This means the world’s central banks are tightening financial conditions and raising interest rates despite economic growth slowing down.

This is a difficult situation for investors. Because inflation is persisting the higher prices are damaging consumer confidence. As a result, we’ve seen companies adjust their outlooks and lose some value as markets now also price in in a potential recession.

Because investors are looking at future earnings, expectations of declining cash flows and profits are usually reflected in falling stock prices. In a bear market, investors become more risk-averse than risk-seeking, and the rush to protect themselves from losses can lead to prolonged declines in share prices.

IS A BEAR MARKET A RECESSION?

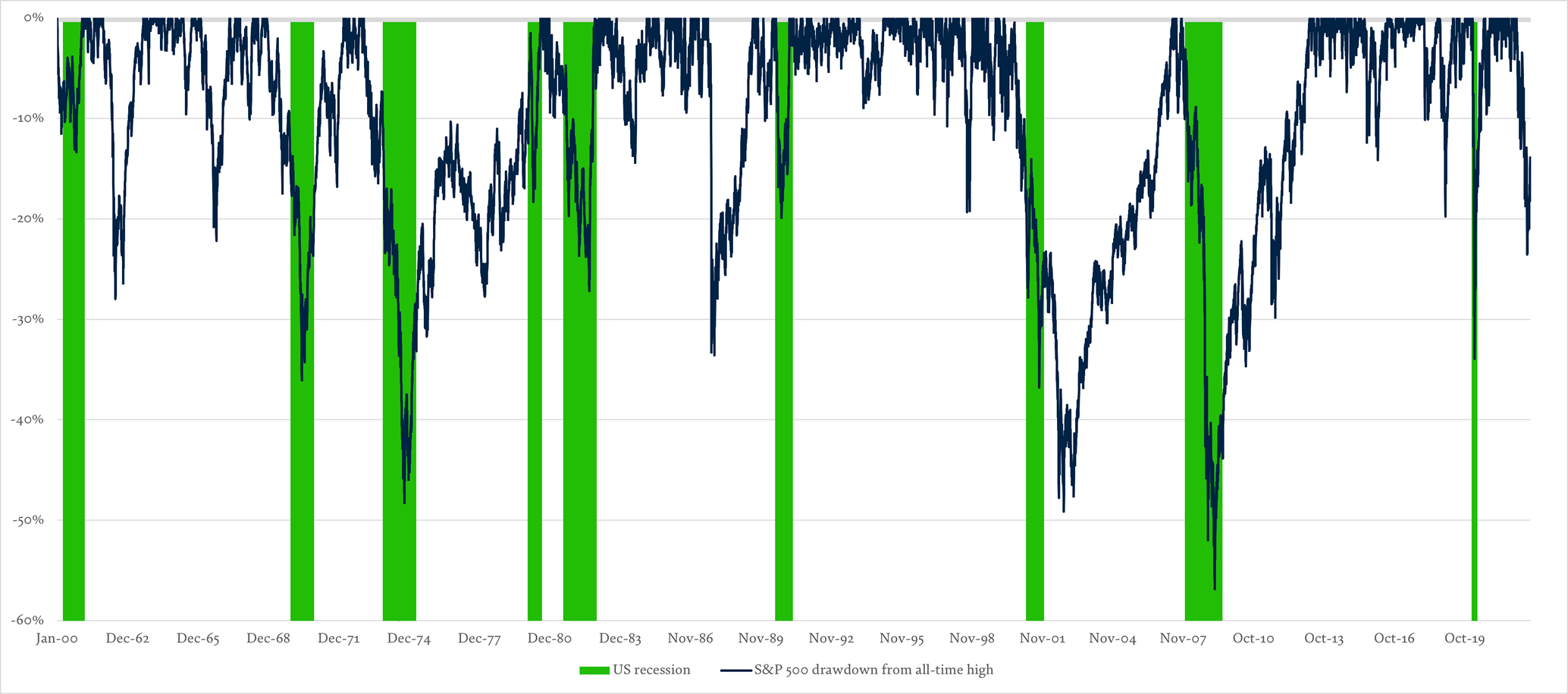

Bear markets often overlap an economic recession, but not always. A look at history reveals that of the 20 bear markets on the S&P 500 since the 1920s, 13 occurred alongside a recession.

What we do see when the two overlap is a bear market that tends to last longer and fall further. Data from the MSCI World Index (a broad global equity index based across 23 markets) suggests that the average bear market involves a drop of 25 per cent and lasts 170 days. When there is no recession, it's 150 days and it drops by around 21 per cent. But when it coincides with a recession, it lasts 260 days and the market falls around 40 per cent. The chart below, which shows drawdowns from the all-time highs (zero), reveals that bear markets that occur outside a recession tend to be shallower and shorter.

Source: Bloomberg/Coutts

The key thing to note is that a bear market is likely to precede or coincide with a recession, rather than react to it. As Coutts UK, Head of Asset Allocation, Lilian Chovin, points out: “The market doesn’t follow the economy. On average, markets trough before the economy because they look forward.”

Another key thing is that every bear is different, adds Lilian. “Sometimes markets bottom out before the recession even starts, sometimes during, sometimes after. Even if you knew the exact dates of the next recession, selling your investments when it starts and buying back when it finishes would actually more likely than not be a losing strategy if history is a guide.”

Coutts Asset Management’s approach to managing funds during these times is centred around using both historic precedent and real-time analysis to understand market trends, mitigate risk and identify opportunities. Because we are always invested, we continuously tilt our investments towards certain sectors and regions based on our assessment of macroeconomics and where the headwinds and tailwinds are.

For example, at the moment we favour healthcare and more defensive sectors, such as utilities and consumer staples, because we believe the economy is going to be challenged, and those areas are best-placed to weather any potential storms.

“If there is a classic recession, and if history is a guide, healthcare is actually attractive because earnings won't fall much,” says Lilian. “They are less impacted than other sectors such as financial services, which can see their earnings fall by 20% on average during a recession”.

WHAT WE CAN LEARN FROM HISTORICAL BEAR MARKETS

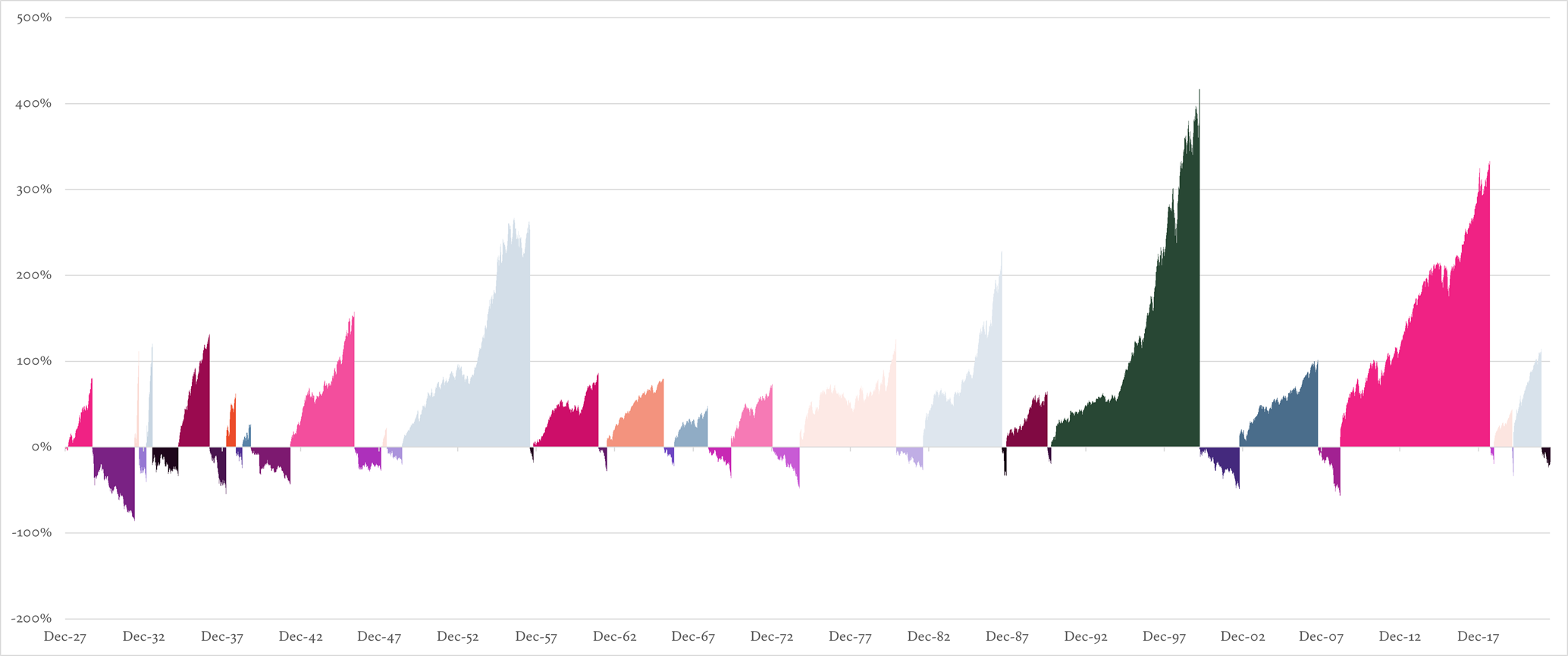

Firstly, bear markets are rare with just 20 in the last 94 years and each one lasting, on average, less than a year. As we can see below, outside of a bear market, markets are generally growing.

Source: Coutts/Bloomberg

You can probably guess which ones were most severe, connected as they were to major economic turmoil – from the collapse of Bretton Woods and the oil crisis in 1973-74, to the dot com bubble bursting in 2000 and the global financial crisis of 2008.

What these events can teach us is that there are two major reasons for the most acute bear markets – a very severe economic recession or very high valuations. We can use these to predict how bad a bear market can be.

The billion dollar question is: how much downside is left? It’s impossible to know for certain, but one useful indicator is to look at the value of companies’ shares during previous bear markets. We can do this by looking at their ‘price-to-earnings (PE) ratio’, which relates a company’s share price to its earnings per share. During a bear market there often comes a point when companies with a low PE ratio are undervalued with too much pessimism. At this point investors will look to come back in to capture this opportunity. When this happens, markets usually stabilise and rise again.

The S&P 500’s current PE ratio (averaged across the index) is approximately 16.7x according to multpl.com and reflects a continuous downward trend since the December 2021 high of 35.96x PE ratio. While it’s still slightly above the historic average of around 16 times, it’s considerably lower than it’s been for a number of years.

Always remember though, that past performance should not be taken as an indication of future performance.

Bear markets can look alarming, but they are also an opportunity. If you're looking at long term investing, valuations are a much larger driving force of long term returns than the current economic outlook. Five-year time horizons can be far more rewarding than 12 month ones. And that means there is value to be had.

As Lilian says, “given what we've seen this year, which is not just markets falling 20% but many stocks getting cheaper by a sizeable amount, there could be an opportunity for investors to get a good deal, and for markets to start recovering”.

The value of investments, and the income from them, can fall as well as rise and you may not get back what you put in. Past performance should not be taken as a guide to future performance.

Coutts’ approach to investing