Investments | 15 February 2022

FINDING STEADY GROUND

January was a challenging month for investors as markets dropped amid worries about Ukraine, higher inflation and interest rates on both sides of the Atlantic.

SHARE

Become a client

When you become a client of Coutts, you will be part of an exclusive networkMarkets have settled for now though, adjusting to the new timescale for rate rises in the US set by the influential US Federal Reserve (Fed). We believe inflation should start to fall again later this year once Covid-related supply chain issues settle down.

After US inflation numbers hit 7% in December, the Fed indicated it was likely to begin increasing interest rates sooner than initially thought, with the first hike expected in March. The announcement raised concerns about the impact of higher rates on the pace of economic growth.

This led to a rotation out of interest rate sensitive growth stocks (companies with above average long-term prospects, such as technology) to value stocks (companies that typically trade at a lower level than they appear to be worth, like energy companies or banks).

NETFLIX CHILLS

Among the hardest hit were tech stocks – particularly younger companies that attracted a lot of interest during the pandemic like Netflix, Zoom or Peloton. But some large companies also saw large price swings, notably Meta (Facebook).

Sven Balzer, Head of Investment Strategy at Coutts, said: “A sell-off in stocks at some point was to be expected as markets had been rising steadily without interruption. The S&P 500, for example, went through a long period without any correction at all – 61 weeks without dropping more than 6% to be precise.

“It’s also not surprising that the growth segment of the market has been the most impacted given such stocks are vulnerable to interest rate changes.”

On the fixed income side of markets, UK and US government bond yields rose (meaning prices fell) as investors looked ahead to higher interest rates. Chinese government bonds, however, produced modest, positive returns in January as China looked set to stimulate its economy. Our Chinese government bond holdings therefore benefitted our own clients’ portfolio performance.

Overall, the MSCI World Index of global equities returned -4.9% in January, while US 10-year Treasury bonds returned -1.9%.

UK AND EUROPE HOLD UP WELL DESPITE HIGH INFLATION

Sven added that there were positives too in terms of market performance.

“The impact on growth stocks did drag down the US market but, in contrast, we’ve seen the UK and Europe – both with higher proportions of value stocks – remain rather resilient,” he said.

Inflation has continued to rise in the UK, and the Bank of England has already started tightening monetary policy with an interest rate hike in December, swiftly followed by another in February 2022. This has taken UK interest rates to 0.5%, and further rises are likely over the rest of this year in a bid to tackle the rising cost of living.

However, the UK stock market performed well in January, better than the US. One of the main reasons is the FTSE 100’s weight of value stocks, in particular energy and financials which make up over a quarter of the index. These businesses have been resilient in the past month against the recent volatility, while other sectors declined. Many active investment managers struggled to maximise returns in this environment.

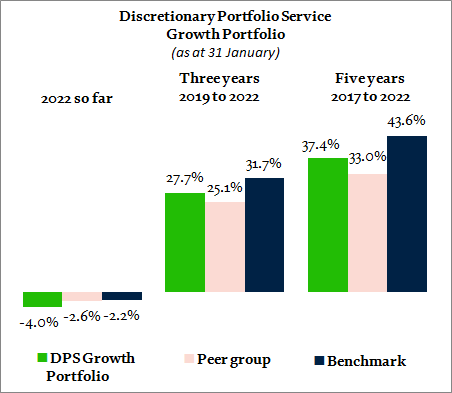

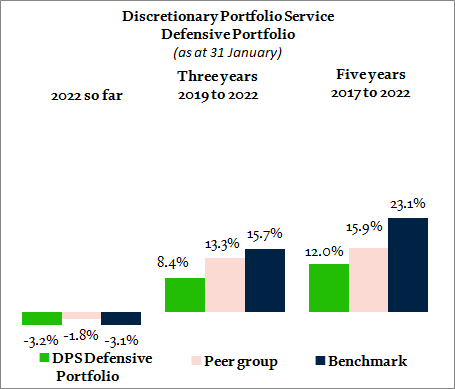

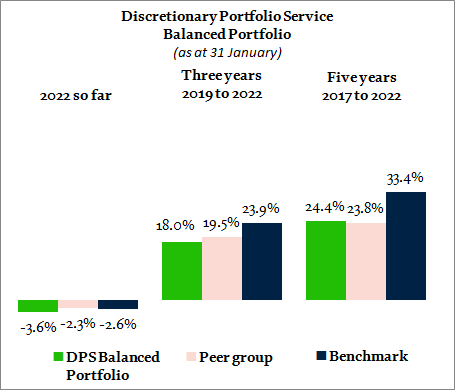

OUR LATEST PERFORMANCE

While our portfolios and funds have not been immune to the market swings we’ve seen so far this year, we continue to see solid performance over the longer term, with our balanced and growth mandates ahead of competitors over five years.

The portfolio performance shown below is net, so has fees and charges deducted, while the benchmark performance is gross with no such deductions.

Data to 31 January 2022. Cumulative returns calculated on sterling basis, including fees, charges and income to 31 January 2022. These data are based on composite performance, individual portfolio monthly returns are asset-weighted based on their respective asset values at the beginning of the month. Peer group returns provided by Asset Risk Consultants (ARC); end-January data represents ARC estimate. Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can go down as well as up and you may not recover the amount of your original investment. Sources: Coutts & Co, ARC. February 2022.

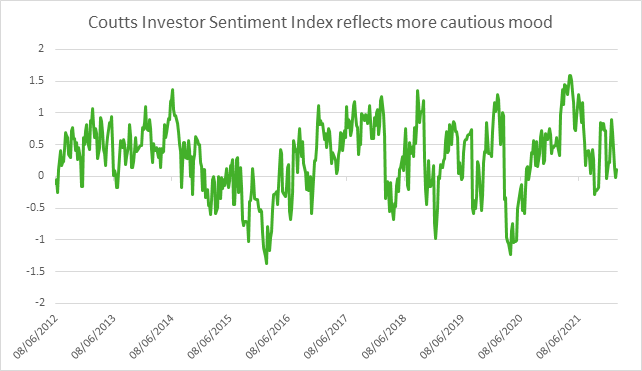

Our measure of the market mood – the Coutts Investor Sentiment Index – fell significantly in January, reflecting a more cautious mood among investors.

Readings over 1 show investor complacency, readings below -1 show anxiety. Our index brings together various key market measures looking at volatility and investor positioning. Source: Coutts, February 2022.

SEIZING OPPORTUNITIES ON OUR CLIENTS’ BEHALF

Here at Coutts, having previously increased the amount of cash we hold in light of current market challenges, we’ve been well positioned to react opportunistically to market swings. And we’ve done just that with two recent changes to our client portfolios and funds.

Firstly, we’ve bought more US stocks. While such stocks could still see more volatility, the amount by which they’ve dropped recently looked overdone compared to the resilient fundamentals of the companies involved, which include some strong financial results.

We’ve also sold more of our investment grade bond holdings and bought UK government bonds instead. There has been a notable rise in government bond yields in the last few weeks as central banks start focusing on inflation. But despite some tough talk, we believe central banks will be mindful not to let yields rise too quickly, and inflationary pressures should ease later this year.

Investment grade bond valuations, on the other hand, look unattractive and could suffer from increasing cost pressures and record-high corporate profitability.

OUR LONG-TERM PERFORMANCE

31/12/2016 - 31/12/2017 |

31/12/2017 - 31/12/2018 |

31/12/2018 - 31/12/2019 |

31/12/2019 - 31/12/2020 |

31/12/2020 - 31/12/2021 |

|

MSCI World (sterling, including income) |

11.8% |

-3.0% |

22.7% |

12.3% |

22.9% |

Coutts Defensive Portfolio |

5.8% |

-3.7% |

8.3% |

3.5% |

1.3% |

Peer group - ARC Cautious PCI |

4.5% |

-3.6% |

8.1% |

4.2% |

4.2% |

Composite benchmark |

5.7% |

-1.6% |

11.1% |

7.7% |

1.7% |

Coutts Balanced Portfolio |

9.1% |

-5.1% |

12.4% |

4.4% |

6.9% |

Peer group - ARC Balanced Asset PCI |

6.7% |

-5.1% |

11.7% |

4.3% |

7.6% |

Composite benchmark |

7.9% |

-2.9% |

14.1% |

6.5% |

7.5% |

Coutts Growth Portfolio |

12.1% |

-6.5% |

16.9% |

4.7% |

12.7% |

Peer group - ARC Steady Growth PCI |

9.4% |

-5.6% |

15.0% |

4.6% |

10.2% |

Composite benchmark |

10.4% |

-4.2% |

17.0% |

4.9% |

13.6% |

Return data for funds are calculated net of fees, in sterling and assumes reinvestment of dividends. Past performance should not be taken as a guide to future performance. Peer group returns provided by Asset Risk Consultants (ARC). Benchmarks represent a static mix of equities and bonds in proportions relevant to each strategy. The value of investments, and the income you get from them, can go down as well as up, and you may not recover the amount of your original investment. Source: Coutts & Co., Asset Risk Consultants (ARC), Morningstar, Refinitiv, February 2022.

Share

CIO Update – Managing risk amid periods of uncertainty | Insights | Coutts Crown Dependencies