Investing & Perfomance | 19 March 2024

Is it time to invest in China?

With Chinese stocks trading at exceptionally good value, is now the right time to buy into the world’s second largest economy? Coutts Multi-Asset Strategist David Broomfield shares his view.

Napoleon is thought to have said “China is a sleeping giant, when she wakes she will shake the world”. Although around 200 years early, he was certainly on to something.

China ‘awoke’ around 1990 and has generated an average annual GDP growth rate of over 9%, with peaks at times exceeding 14%, according to data from the World Bank.

More recently though, growth rates have slowed, and China’s stock markets have reflected this in no uncertain terms.

The CSI 300 – which includes the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges – has fallen around 40% since its peak in 2021.

Coutts current view of China

At Coutts we’re currently neutral on Chinese stocks. This is because of structural challenges sitting behind China’s stock market drop, and the state intervening in markets to spend excess cash from a huge trade surplus.

For us, this doesn’t represent a very solid foundation on which to grow. So much depends on the state’s market intervention rather than the underlying fundamentals, such as company earnings and economic growth.

Also, the country’s economic expansion isn’t translating through to stock market performance efficiently enough in our view. More on that later…

Chinese stocks could be offering unprecedented value

Many commentators suggest China could currently represent unprecedented value.

Let’s stick with the CSI 300 and look at its average price-to-earnings ratio. This well-known measure of whether a business or market is under or over-valued looks at a company’s stock price compared to its overall earnings. The higher the ratio, the more expensive a stock is considered to be in relation to the money the company’s making.

The CSI 300 is currently trading at an average price-to-earnings ratio of around 13, our own analysis shows. This is really pretty low – much lower than most other major markets and around half the equivalent number for the S&P 500 in the US.

The value of investments, and the income from them, can fall as well as rise and you may not get back what you put in. Past performance should not be seen as an indication of future performance. You should continue to hold cash for your short-term needs.

So what’s the catch?

Things are hardly ever as simple as they seem when it comes to markets. And if Chinese stocks are very cheap at the moment, we should ask ourselves why. We need to look at what’s caused recent lacklustre economic growth in China.

The two main arguments for the Chinese stock market falling over the last couple of years are the politicisation of the country’s economy and its deep structural challenges, which include over-reliance on property investment to mop up high savings rates.

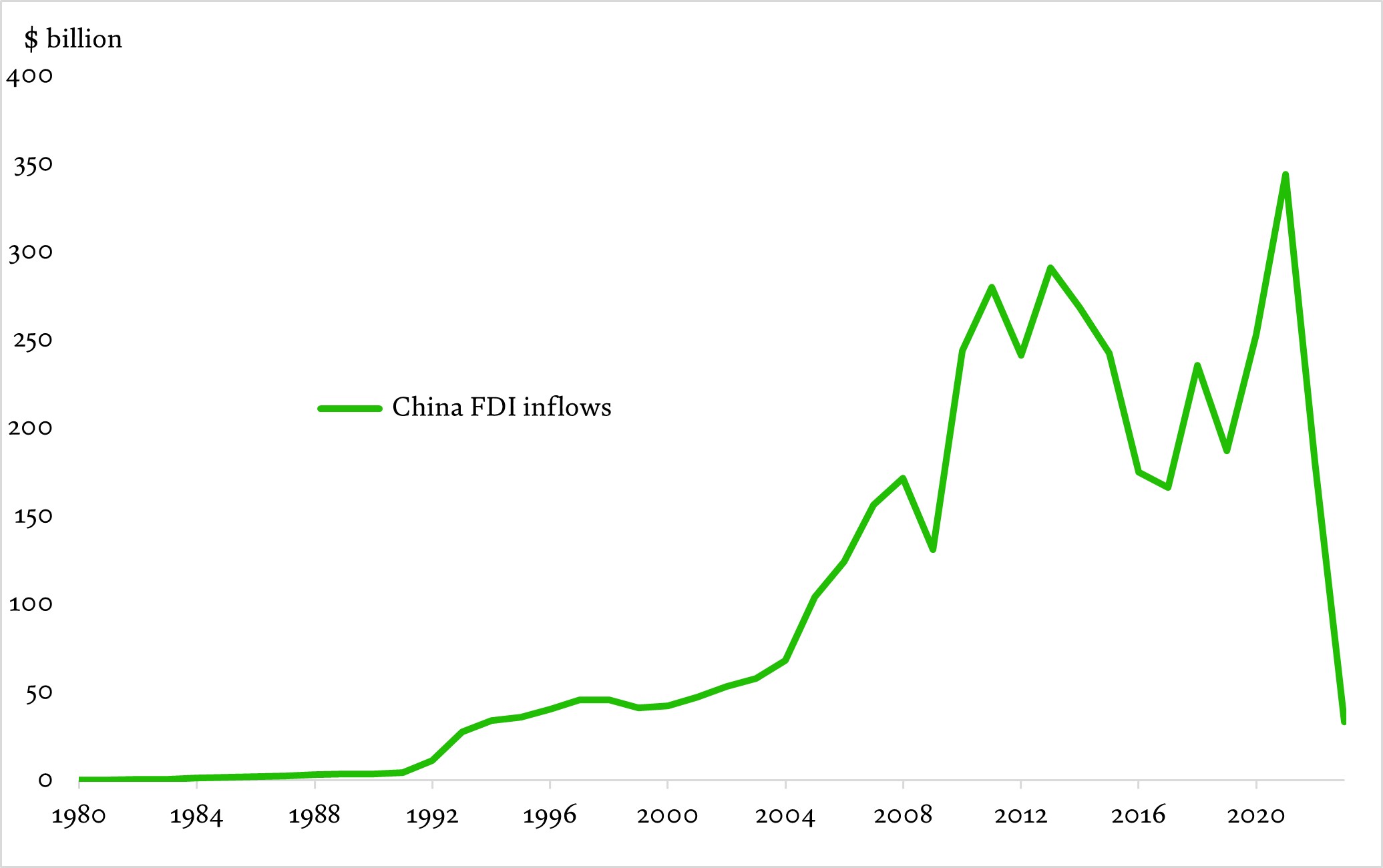

Foreign Direct Investment in China – when an international investor acquires a meaningful stake in a Chinese company or project – has seen a huge fall since the start of 2022.

Foreign direct investment in China collapsed in 2023

Source: State Administration of Foreign Exchange (China), March 2024

This gives some credence to the ‘politicisation’ argument. A parallel spike in geopolitical tensions over the same period – China’s rhetoric on Taiwan and cordial bilateral relations with Russia and North Korea – have made investors more cautious.

We’ve also had abrupt regulatory shifts. These include Beijing's closure of foreign consultancy and due diligence firms, and crackdowns on tech firms alongside new national security rules on cross-border data.

This all goes some way to explaining the lack of investment flows into China.

But it’s worth noting that investing directly in mainland China is still a relatively recent phenomenon anyway. Foreign investment has only been allowed to flow meaningfully into China since 2016, and only since 2020 have those flows been allowed to flow relatively unrestricted to mainland capital markets.

China’s enormous current account

So what about these aforementioned structural challenges? China runs a huge trade surplus. The US runs a huge trade deficit. The world has been running this imbalance for multiple decades.

Essentially the proceeds from Chinese exports become excess savings which ultimately get exported to and invested in the rest of the world – on an unprecedented scale.

These flows are driven by the Chinese government and used to bolster their reserves, usually by buying US government bonds.

But as China has grown, it has shifted this enormous current account surplus – the difference between its exports and imports – into giant infrastructure and green energy projects in an effort to stimulate economic growth.

The structural issue has come about because China’s current account surplus and extremely high domestic savings rate flooded the domestic economy with liquidity. And without enough domestic demand to absorb it, China’s banks ended up directing huge sums into fuelling what became the country's property market bubble.

Those gigantic property development projects accounted for about a quarter of the country’s economic activity… until the bubble burst.

China – does stellar growth translate to solid returns?

All this is contributing to a certain lack of efficiency in China. Those investing in the country’s stock markets want to participate in a broad-based economic growth story fuelled by corporate earnings growth.

But here’s the reality. From the start of 2002 to the end of 2023, the CSI 300 returned 6.4% annualised, including dividends reinvested. This is against an economic backdrop of quite stellar 8.8% annualised real GDP growth, according to World Bank data. The equivalent US numbers show that the S&P 500 returned 8.7% against economic growth of just 2.5%.

So GDP growth clearly translates much more efficiently into equity returns in the US than it does in China. Your willingness to participate in China’s future economic growth story is therefore key to making a decision about investing there.

In a nutshell, China is certainly cheap right now, but it’s worth considering all the factors behind that when deciding whether or not to invest.

Hear David discussing China in our latest Need to Know investment podcast.

This article should not be taken as investment advice.

The above article has been written and published by Coutts Crown Dependencies investment provider, Coutts.

Share

More insights